Vietnam’s Trade & Currency Under Pressure as Strait of Hormuz Crisis Drives Oil Above $100: Data-Driven Analysis

Vietnam’s trade & currency face pressure as the Strait of Hormuz crisis pushes oil above $100. Explore data-driven insights, risks, & economic impact.

Introduction: A Perfect Storm for Emerging Asia

The global economy is once again being reshaped by geopolitics. The ongoing 2026 conflict involving Iran, the United States, and Israel has triggered a severe disruption in one of the world’s most critical energy arteries: the Strait of Hormuz. This narrow maritime chokepoint, responsible for transporting roughly 20% of global oil supply, has seen near-total disruption in shipping flows. The immediate consequence has been a rapid surge in oil prices, with Brent crude crossing the $100 per barrel threshold for the first time in four years, and at times spiking as high as $126. Despite Vietnam's physical distance from the US, Israel, and Iran confrontation, economic ties to international oil markets & aviation routes imply that spillovers are already occurring, which can further impact the Vietnam import data & Vietnam export data.

While this is a global shock, its effects are highly uneven, impacting the global trade data. Emerging Asian economies, especially those heavily dependent on imported energy, are bearing the brunt. Among them, Vietnam stands out as a particularly interesting case. The country combines strong export-led growth with increasing energy dependence, making it vulnerable to both trade disruptions and currency instability. This blog examines how the Hormuz crisis is putting pressure on Vietnam’s trade balance and currency, using data-driven insights to unpack the evolving risks.

The Strait of Hormuz Crisis: Why It Matters

The Strait of Hormuz is not just another shipping route. It is the single most important energy chokepoint in the world, facilitating the movement of around 20 million barrels of oil per day.

Since late February 2026, escalating military tensions have led to:

-

A 70% drop in tanker traffic, eventually falling close to zero

-

Attacks on commercial vessels

-

Suspension of shipping operations by major trade firms

-

A spike in war-risk insurance premiums

This has effectively created a supply shock reminiscent of the 1970s oil crisis. Analysts describe it as the largest disruption to global energy markets in modern history.

Oil Price Transmission Effects

Oil prices have surged rapidly due to:

-

Physical supply constraints

-

Panic buying and speculative trading

-

Strategic stockpiling by governments

-

Supply chain rerouting costs

As a result, the global economy is experiencing:

-

Rising inflation

-

Slower growth

-

Currency volatility

-

Increased risk premiums

Vietnam’s Structural Vulnerability to Oil Shocks

Vietnam is often seen as one of Asia’s strongest growth stories, with GDP growth projected at 8.2% for 2026 under normal conditions. However, this growth model comes with structural vulnerabilities:

1. Energy Dependence

Although Vietnam produces some crude oil, it is increasingly reliant on imported refined fuels to meet domestic demand. This exposes the economy to global price fluctuations.

2. Export-Led Growth Model

Vietnam’s economy is heavily dependent on manufacturing exports, particularly in:

-

Electronics

-

Textiles

-

Machinery

Higher energy costs directly increase production expenses, reducing competitiveness.

3. Trade Balance Sensitivity

Vietnam typically runs a trade surplus, but rising energy imports can quickly erode this advantage.

Oil Above $100: Quantifying the Economic Impact

The relationship between oil prices and Vietnam’s macroeconomic performance is well documented. According to MUFG estimates:

-

Every $10 increase in oil prices:

-

Cuts GDP growth by 0.2 percentage points

-

Raises inflation by 0.3–0.4 percentage points

Scenario Analysis

Let’s consider three scenarios:

Scenario 1: Oil stabilizes at $80–90

-

Minimal disruption

-

GDP remains near 8%

-

Inflation manageable

Scenario 2: Oil sustained at $100+

-

GDP falls below 7.5%

-

Inflation rises sharply

-

Trade balance deteriorates

Scenario 3: Oil spikes to $120+

-

Severe stagflation risk

-

Significant currency depreciation

-

Policy tightening required

These projections highlight how sensitive Vietnam’s economy is to energy shocks.

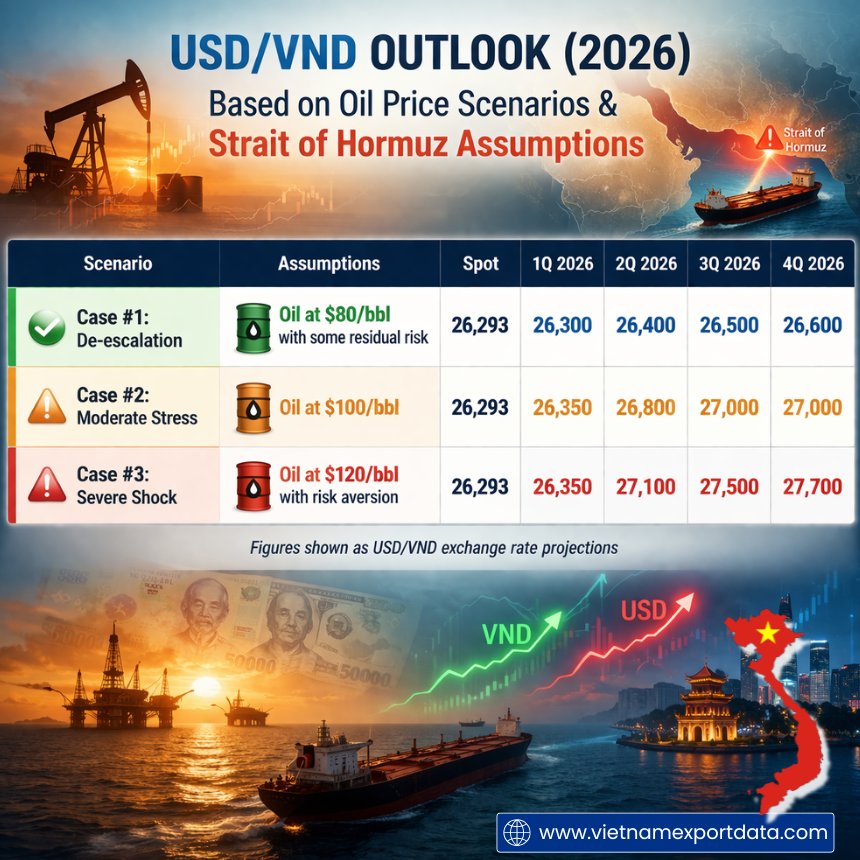

Currency Pressure: The Vietnamese Dong Under Stress

One of the most immediate effects of the crisis is on Vietnam’s currency, the Vietnamese dong (VND).

Exchange Rate Dynamics

Analysts forecast:

-

Baseline (de-escalation): USD/VND 26,300–26,600

-

Oil at $100: USD/VND 27,000

-

Oil at $120+: USD/VND could reach 27,700+

Why the Dong is Weakening

Several factors are contributing to currency pressure:

1. Widening Trade Deficit

Higher oil import costs increase demand for foreign currency, especially USD, impacting the Vietnam customs import data of oil.

2. Capital Outflows

Investors may shift funds to safer assets amid global uncertainty.

3. Interest Rate Differentials

Rising US rates combined with domestic pressures weaken the dong.

4. Inflation Expectations

Higher inflation reduces the real value of the currency.

Real-World Signal

Recent reports indicate that persistent high oil prices and trade deficits are already weighing on the VND, with markets closely watching the USD/VND trajectory.

USD/VND Outlook Based on Oil Price Scenarios & Strait of Hormuz Assumptions (2026)

Trade Impact: From Surplus to Strain

Vietnam’s trade engine is now facing multiple pressures simultaneously.

Rising Import Costs

Energy imports are becoming significantly more expensive:

-

Oil prices up 30% year-to-date

-

Fuel import bills are rising sharply

Export Competitiveness

Higher energy costs affect:

-

Manufacturing margins

-

Pricing competitiveness

-

Supply chain efficiency

This is particularly critical for Vietnam, which competes with countries like:

-

China

-

India

-

Bangladesh

Shipment Disruptions

The Hormuz crisis is also affecting global shipping:

-

Longer routes

-

Higher freight costs

-

Delays in supply chains

This further increases the cost of trade.

Inflation and Domestic Economic Stress

Vietnam’s inflation outlook is deteriorating as energy prices rise.

Inflation Trends

-

Pre-crisis inflation: 2.5%

-

Post-crisis projection: 4%

Transmission Channels

Inflation is being driven by:

-

Fuel prices

-

Transportation costs

-

Food prices (via fertilizer disruptions)

-

Imported inflation

Globally, the crisis is also disrupting fertilizer and chemical supply chains, further pushing up food prices.

Policy Response: Vietnam’s Strategic Moves

The Vietnamese government is already taking steps to mitigate the crisis.

1. Fuel Tax Cuts

Vietnam is considering:

-

Reducing fuel import tariffs to zero

-

Stabilizing domestic energy prices

2. Supply Diversification

Efforts include:

-

Securing alternative oil sources

-

Increasing strategic reserves

3. Monetary Policy Tightening

Higher oil prices may force:

-

Interest rate hikes

-

Liquidity tightening

Analysts suggest interbank rates could rise from 7.5% to around 9% under sustained high oil prices.

Broader Emerging Market Context

Vietnam is not alone. The Hormuz crisis is triggering a wider emerging market shock.

Regional Impact

-

Japan & South Korea: Currency stress and rising manufacturing costs

-

India: Oil import vulnerability, policy focus on supply security

-

Sri Lanka & Southeast Asia: Fuel shortages and rationing

Inflation Shock

Emerging markets could see:

-

+0.8–1.0 percentage point increase in inflation

This reinforces the idea of a global energy risk premium, disproportionately affecting oil-importing economies.

Long-Term Structural Implications

Beyond the immediate crisis, several long-term trends are emerging.

1. Shift Toward Energy Diversification

Countries are accelerating:

-

Renewable energy investments

-

LNG diversification

-

Strategic stockpiling

2. Supply Chain Reconfiguration

Companies may:

-

Relocate production

-

Diversify sourcing

-

Reduce reliance on volatile regions

3. Currency Realignment

Persistent shocks could lead to:

-

Structural weakening of emerging market currencies

-

Greater USD dominance

Vietnam Trade Data Snapshot: How Energy Shock Is Reshaping Flows

To understand the real impact of the Strait of Hormuz crisis, it helps to look at Vietnam’s latest trade structure and how sensitive it is to energy costs and external demand.

Vietnam’s Trade Structure at a Glance

Vietnam remains one of Asia’s most trade-dependent economies:

-

Total trade (exports + imports): $900+ billion annually

-

Exports (2025): $455 billion

-

Imports (2025): $475 billion

-

Trade surplus: $20-30 billion

This surplus has been a key pillar supporting the Vietnamese dong and macro stability.

Key Export Sectors (Highly Energy-Sensitive)

Vietnam’s top export categories include:

-

Electronics & components (30%+ of exports)

-

Machinery & equipment

-

Textiles & garments

-

Footwear

These sectors are:

-

Energy-intensive

-

Highly dependent on global demand

-

Sensitive to shipping and trade costs

As oil prices rise, production and freight costs increase, directly affecting export margins.

Import Composition: Where the Pressure Builds

Vietnam’s import basket reveals why oil shocks matter so much:

-

Machinery & equipment: 30%

-

Electronics components: 25%

-

Petroleum products & energy inputs: 8–10%

-

Raw materials (plastics, chemicals, metals): significant share

Even though direct oil imports seem modest, energy costs are embedded across:

-

Industrial inputs

-

Transportation

-

Manufacturing supply chains

This means the true exposure to oil prices is much higher than headline numbers suggest.

Energy Import Dependency: A Critical Weak Point

One of the most important data points often overlooked:

-

Around 85% of Vietnam’s crude oil imports come from the Middle East, as per Vietnam crude oil imports by country.

This creates a direct vulnerability to the Strait of Hormuz disruption.

In practical terms:

-

Supply disruptions lead to immediate import stress.

-

Higher oil prices result in a rising import bill.

-

Both pressure on the trade balance and currency.

Monthly Trade Trends: Early Signs of Stress

Recent monthly trade patterns already hint at emerging pressure:

-

Export growth is slowing due to weaker global demand and rising costs.

-

Import values are rising, driven partly by higher energy prices.

-

The trade surplus is narrowing compared to previous peaks.

If oil remains above $100:

-

Import growth (value-driven) will likely outpace export growth.

-

Vietnam could see a temporary shift from surplus to deficit.

Trade Balance Sensitivity to Oil Prices

A simplified way to understand the impact:

-

A 10–20% increase in energy import costs can reduce Vietnam’s trade surplus by several billion dollars

-

Sustained oil above $100 could:

-

Cut surplus significantly

-

Increase demand for USD

-

Accelerate VND depreciation

This aligns closely with the currency scenarios discussed earlier.

Risks Ahead: What Could Make Things Worse?

Several downside risks remain:

1. Prolonged Strait Closure

A sustained blockade could keep oil above $100–120.

2. Escalation of Conflict

Further attacks on energy infrastructure could worsen supply shortages.

3. Financial Market Spillovers

Global risk aversion could trigger capital flight from emerging markets.

4. Policy Constraints

Limited fiscal and monetary space could restrict Vietnam’s response.

Key Takeaways

The latest Vietnam trade report reinforces a central theme of this blog: Vietnam is not just facing an oil price shock, but a multi-layered macroeconomic stress event.

The three biggest risks identified are:

-

Energy supply disruption, not just price increases

-

Sharp currency depreciation under sustained oil pressure

-

A reversal of the trade surplus, weakening external stability

In short, the Strait of Hormuz crisis could push Vietnam from a position of strength into a more fragile macroeconomic environment much faster than traditional models would suggest.

Conclusion: A Stress Test for Vietnam’s Economic Model

In conclusion, the Strait of Hormuz crisis is more than just an energy shock. It is a full-scale stress test for Vietnam’s economic model.

At its core, the crisis exposes a fundamental tension:

-

Vietnam’s growth depends on global trade and stable energy costs

-

But its increasing integration into global supply chains makes it vulnerable to external shocks

With oil prices above $100, the country faces a combination of:

-

Slower growth

-

Higher inflation

-

Currency depreciation

-

Trade pressures

The data suggests that if current conditions persist, Vietnam could transition from a high-growth, low-inflation economy to a more fragile, stagflation-prone environment.

Yet, the situation is not without opportunity. The crisis could accelerate:

-

Energy diversification

-

Structural reforms

-

Supply chain resilience

In that sense, Vietnam’s response in 2026 may shape not just its short-term stability but its long-term economic trajectory in an increasingly volatile global landscape.

Note For Our Readers

We hope this data-driven analysis of Vietnam’s trade and currency pressures amid the Strait of Hormuz crisis helped you clearly understand how global energy shocks translate into real economic stress on the ground. Beyond the headlines of oil crossing $100, the key takeaway is how deeply Vietnam’s growth model is linked to external factors like energy imports, global shipping routes, and currency flows. When these variables shift, the impact is not isolated. It spreads across trade balances, inflation, manufacturing competitiveness, and the stability of the Vietnamese dong.

If you want to go deeper, you can explore Vietnam’s import-export data by country, product, HS code, monitor monthly trade flows, analyze energy import dependencies, or track how currency movements are affecting different industries using advanced trade intelligence tools from VietnamExportdata. For more detailed insights, including customized trade reports, sector-specific data, and tailored market analysis for your business needs, feel free to reach out to us at [email protected] today.

Share

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0