Vietnam Rice Exports in 2025 seen falling 11.5% due to the Philippines Import Ban

Vietnam rice exports are projected to fall 11.5% in 2025 as the Philippines imposes an import ban, reshaping trade flows, prices, & market strategy.

Vietnam’s rice export industry is entering one of its toughest years in recent memory. Forecasts from industry officials show that total shipments in 2025 will fall by about 11.5 percent, settling at about 8 million metric tons. For a country that has built a global reputation as one of the world’s most reliable rice suppliers, this marks a significant setback. According to the Vietnam export data and the Vietnam customs export data of rice, the total value of Vietnam rice exports reached around $3.59 billion in the first ten months of 2025.

The main driver is the decision by the Philippines to halt rice imports beginning in September 2025. The ban was introduced to stabilize farmgate prices and calm a domestic market shaken by low palay prices and farmer protests. The ban hit Vietnam harder than any other supplier because the Philippines has long been Vietnam’s number one customer, often absorbing more than 40 percent of its total rice exports. Vietnam is the 3rd largest rice exporter in the world, according to global trade data.

This blog takes a deep and data-grounded look at why exports are falling, how the ban has disrupted regional trade, what this means for Vietnamese farmers and exporters, and how Vietnam is trying to pivot. The story encompasses price swings, global competition, domestic restructuring, and shifting consumption patterns across Asia and Africa. The result is a complex picture of a major agricultural economy under pressure, but also one with room to adapt and evolve.

The Scale of the Decline: What the Numbers Show

In the first eight months of 2025, Vietnam shipped & exported roughly 6.37 million tons of rice, worth more than $3.26 billion. Export volume edged up slightly from the year before, but revenue fell by more than 15 percent. That drop in value came from falling global rice prices and a sharp slowdown in buying activity.

By the end of the first ten months, the impact of the Philippines import ban became unmistakable. Vietnam rice exports to Philippines fell to about 2.96 million tons, a decline of more than 18% compared with the same period in 2024. Some Vietnamese industry groups reported an even deeper decline of around 27% in shipments to that market. The reduction was so large that it pulled down Vietnam’s entire export forecast for the year.

Prices told the same story. Vietnam’s benchmark 5% broken rice dropped from about 389 dollars per ton in August to about 372 dollars in September. Year on year, prices were down more than 30%. Fragrant rice, which usually sells at premium levels, hit its lowest price in nearly three years, as per the data on Vietnam rice exports by HS code. This type of rice has always been a strong performer for Vietnam, so the slump carried extra weight.

When an exporting country loses its biggest customer almost overnight, the shock ripple spreads across every part of its supply chain. Rice mills slow their buying. Farmers hesitate to release stocks. Exporters scramble to find alternative markets. All of these effects appeared in Vietnam during the second half of 2025.

Vietnam’s Rice Exports in 2025: What the Data Says

Overview

-

In 2025, estimates suggest that Vietnam could export around 8 million tons of rice, down about 11.5 percent from previous expectations.

-

By the end of October 2025 (first 10 months), actual exports reached approximately 7.2 million tons, with a total export value of about USD 3.7 billion.

-

For comparison: during the first eight months of 2025, Vietnam exported roughly 6.37 million tons, valued at USD 3.26 billion.

-

By the first nine months of 2025, Vietnamese rice exports had reached about 6.82 million tons, earning USD 3.48 billion.

These numbers show, despite varied monthly performance, that 2025 is shaping up as a challenging year for Vietnam’s rice trade.

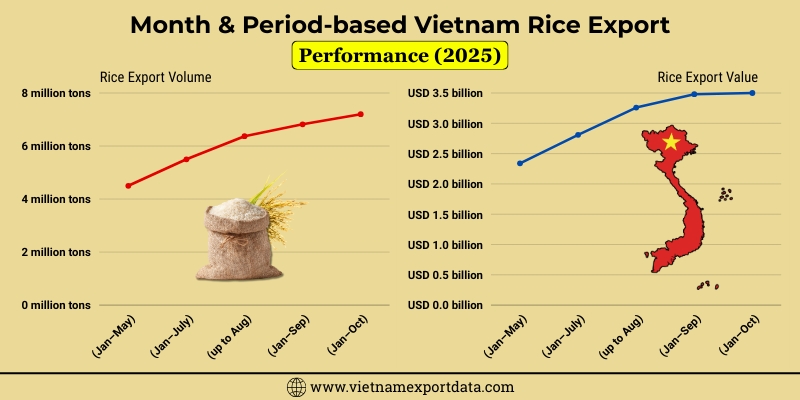

Month & Period-based Vietnam Rice Export Performance (2025)

|

Period / Indicator |

Rice Export Volume (tons) |

Export Value (USD) |

Average Export Price (US$/ton) |

|

First 5 months (Jan–May) |

4.5 million tons |

USD 2.34 billion |

US$516.4/t (or US$0.516/kg) |

|

First 7 months (Jan–July) |

5.5 million tons |

USD 2.81 billion |

US$514/t |

|

First 8 months (up to Aug) |

6.37 million tons |

USD 3.26 billion |

(implied earlier in the year before the larger dip) |

|

First 9 months (Jan–Sep) |

6.82 million tons |

USD 3.48 billion |

US$509/t (noted for the 9-month average) |

|

First 10 months (Jan–Oct) |

7.2 million tons |

USD 3.5 billion |

US$511/t (average price over 10 months) |

What this shows: Volume of shipments remained moderately strong during much of 2025, but the value fell significantly compared with 2024, indicating lower prices, possibly lower margins, and increased market pressure.

Why the Philippines Imposed the Rice Import Ban

The Philippines introduced the ban to address falling palay prices that had fallen below production costs in some regions. A series of large import arrivals earlier in the year had pushed down local prices for unhusked rice. Farmers complained that they were losing money on each harvest. With the wet season crop coming in, pressure mounted on the government to intervene.

The ban was originally intended to last for 60 days. It was then extended to cover the rest of 2025. Political leaders said the extension was essential to protect farmers. Whether this policy will continue into 2026 remains uncertain, but the timing has already reshaped Vietnam’s export year.

The Philippines typically buys between 3 and 3.5 million tons of rice from Vietnam each year, as per the customs data on Philippines rice imports from Vietnam by HS code. At times, the Philippines has accounted for almost half of all Vietnamese rice exports. In 2024, Vietnam exported rice worth $2.61 billion to the Philippines, as per the Vietnam customs data. Losing that volume placed Vietnam in a difficult position, since no single replacement market can absorb such large quantities at short notice.

Key Market Shifts: Who’s Buying & Who Has Pulled Back

The Role of the Philippines

-

In the first 8 months of 2025, the largest buyer was the Philippines, with nearly 2.9 million tons, roughly 45.9% of Vietnam’s total exports in that period.

-

But the Philippines imposed a temporary rice import ban starting September 2025. That significantly disrupted trade flows.

-

According to customs data, shipments to the Philippines fell about 27% year-on-year (for the first ten months) to about 2.96 million tons.

Losing such a large portion of its rice export market in mid-year placed heavy pressure on Vietnam’s overall export performance.

Rise of New Buyers: Africa and Beyond

With traditional buyers pulling back, exports shifted toward alternative markets:

-

In 2025, countries such as Ghana and Côte d’Ivoire saw especially strong growth: exports to Ghana rose approximately 47.3%, and to Côte d’Ivoire nearly 94.5% compared with previous periods.

-

As traditional Asian buyers like the Philippines, Indonesia, or Malaysia cut purchases, demand from Africa, the Middle East, and South Asia became more critical for Vietnamese exporters.

Nonetheless, even this “diversification” was not enough to fully offset the loss, partly because these alternative markets often buy lower-margin rice varieties.

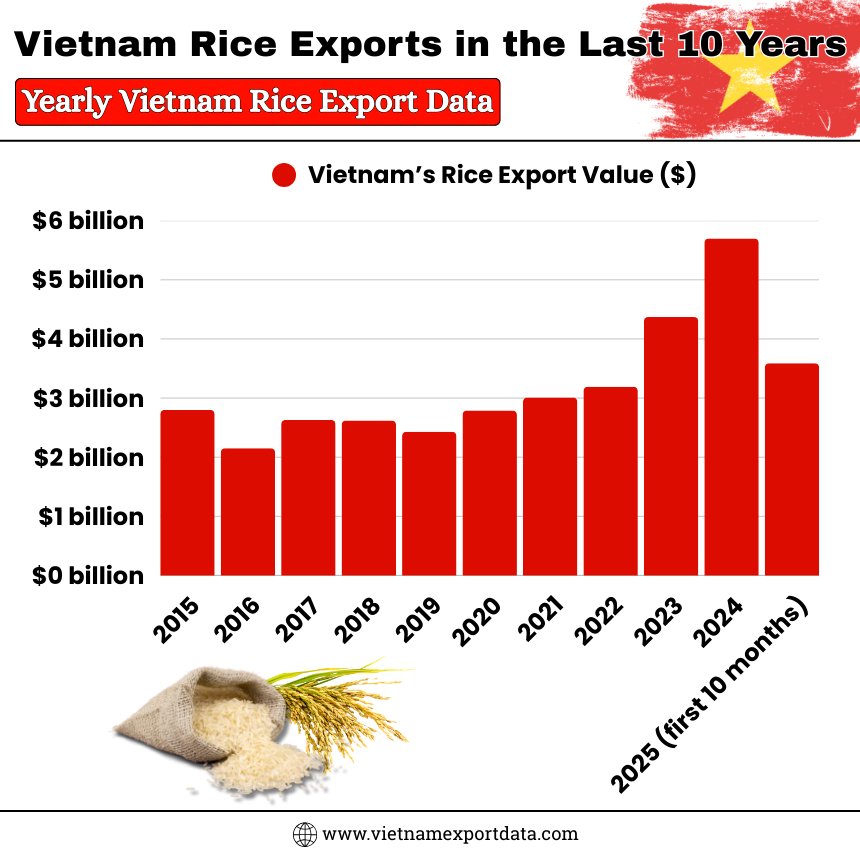

Vietnam Rice Exports in the Last 10 Years: Yearly Vietnam Rice Export Data

|

Year of Exports |

Vietnam’s Rice Export Value ($) |

|

2015 |

$2.80 billion |

|

2016 |

$2.15 billion |

|

2017 |

$2.63 billion |

|

2018 |

$2.62 billion |

|

2019 |

$2.43 billion |

|

2020 |

$2.79 billion |

|

2021 |

$3.01 billion |

|

2022 |

$3.19 billion |

|

2023 |

$4.37 billion |

|

2024 |

$5.70 billion |

|

2025 (first 10 months) |

$3.59 billion |

Price Trends: The Hidden Story

One of the biggest pressures on Vietnam’s rice export value in 2025 came from falling prices.

-

The average export price during the first five months fell to about US$516.4 per ton, down roughly 18.7 percent compared with the same period in 2024.

-

By the first seven months, price levels hovered around US$514/ton.

-

For the first 10 months, the average export price was about US$511/ton, down about 18.5 percent compared with 2024.

-

By September 2025, after the ban, some exporters reported prices for certain Vietnamese rice grades falling to as low as roughly US$380–450/ton, depending on variety and quality.

These price drops significantly reduced export revenue, even when volume remained fairly high.

Implications: What the Data Means for Stakeholders

For Vietnamese Exporters and Farmers

-

Revenue squeeze: Even with close to 7–8 million tons exported in 2025, the total export value is significantly down compared with 2024, because of a lower average price per ton.

-

Cash-flow stress: Exporters must hold larger stocks waiting for buyers. Lower prices reduce margins.

-

Supply-side pressure: Falling prices in export markets likely depressed domestic farmgate prices, hurting farmers’ income. Some are reportedly reconsidering planting decisions, especially with uncertainty about future demand.

For Vietnam’s Export Strategy

Given the disruption, Vietnamese policymakers and industry groups are turning to structural shifts:

-

A push toward higher-quality and value-added rice (e.g., fragrant rice, packaged rice, branded rice) instead of bulk commodity rice.

-

Large-scale market diversification, aiming to reduce dependency on a handful of traditional buyers. Countries in Africa, the Middle East, and South Asia are becoming more prominent.

-

Strategic long-term plans to reduce over-reliance on rice exports. In areas like the Mekong Delta, some farmers are being encouraged to shift to aquaculture or other crops.

The Search for New Markets

With exports to the Philippines falling fast, Vietnamese traders looked elsewhere to offload stocks. Africa became the most promising growth area. Countries like Ghana and Côte d’Ivoire increased imports significantly. Ghana’s purchases were estimated to have grown by more than 45 percent, while Côte d’Ivoire’s imports nearly doubled.

Demand also strengthened in several Middle Eastern countries, where population growth and changing consumption patterns continue to push up rice purchases. South Asia and China also remained steady buyers, although not at levels that could replace the lost Philippine volumes. Even with this diversified demand, exporters struggled to match the certainty and scale that the Philippines had provided. Large buyers offer predictable contracts, which stabilize the market. Without them, trading becomes more scattered and price sensitive.

Another challenge came from the type of rice that each market prefers. African and Middle Eastern countries often buy lower-grade and competitively priced varieties. These markets do not fully replace the value lost when fragrant or higher-quality rice sales fall. Vietnamese exporters said that even when total volume held up, total revenue did not, because the product mix shifted toward lower value varieties.

Global Competition and Price Pressure

While the Philippines import ban was the spark, global market conditions supplied the fuel. In 2025, overall demand softened, and supply from other major exporters increased. India, which had previously restricted some rice exports, regained strength in global markets. Once India returned to more active exporting, it immediately pushed down prices for several rice categories.

Thailand also became more aggressive with pricing. Countries in Africa and the Middle East often choose suppliers based on small price differences, so even a $5 to $10 price gap can redirect entire shipments. Vietnam, which usually prices its fragrant rice above Indian and Thai equivalents, faced difficulty defending its market share under these conditions.

The result was a combined hit. Lower demand from the largest buyer collided with lower international prices and fiercer competition. Even though global rice consumption remains strong, the immediate supply balance is weighed against Vietnam.

Domestic Impact on Farmers and Exporters

The downturn has placed pressure on Vietnam’s rice sector at several levels.

Lower Farmgate Prices

As export prices fell, domestic traders reduced the price they were willing to pay farmers. This squeezed incomes in the Mekong Delta, which is the country’s rice heartland. Many farmers rely on export markets because domestic demand cannot absorb their surplus.

Reduced Cash Flow for Exporters

Exporters depend on rapid turnover to maintain liquidity. The sudden slowdown in shipments meant longer holding times for inventory. That increased storage costs and credit burdens.

Production Choices

Reports from the delta indicate that some farmers may scale back rice planting for the next season. Others may switch to alternative crops or aquaculture, especially shrimp, which has become increasingly profitable in salinity-affected areas. This shift aligns with long-term government strategies but adds complexity to short-term market adjustments.

Vietnam’s Strategy Shift: From Volume to Value

Vietnamese officials have said repeatedly in recent months that the country needs to reduce its reliance on large volume, low margin rice exports. The 2025 downturn has accelerated this discussion.

The Vietnam Food Association and the Ministry of Agriculture have both encouraged a pivot toward high-quality rice. This includes fragrant varieties, soft premium rice, and value-added products like packaged rice with branding. These products can earn higher prices and reduce the country’s dependence on bulk commodity markets that fluctuate rapidly.

Officials have also raised the possibility of reducing the overall rice planting area, especially in regions facing climate pressure. The Mekong Delta is vulnerable to saltwater intrusion, drought, and unpredictable monsoon patterns. Redirecting some land to aquaculture or fruit crops could increase farmer income while lowering the pressure to push high rice export volumes every year.

Can Diversification Solve the Problem?

Market diversification is now the core strategy. Vietnam already ships rice to about 150 countries, but a large share of its volume has traditionally gone to a handful of Asian buyers. The Philippines, Indonesia, China, and Malaysia have been the pillars. When one pillar falls, the system shakes.

Expanding deeper into Africa, the Middle East, and South Asia can provide more balance. These markets offer growing populations and consistent demand. However, they also tend to be price-driven, which limits profit margins.

This is where quality improvement becomes crucial. If Vietnam can supply higher-grade rice that commands premium prices, it can maintain export revenues even if total volume declines. Several exporters say they are investing more in processing technology, quality sorting machines, and branding. The goal is to make Vietnamese rice recognizable and trusted, rather than just interchangeable with cheaper competitors.

What 2026 Might Look Like for Vietnam Rice Exports

There are several clear scenarios for the year ahead.

Scenario One: The Philippines Lifts the Ban

If the Philippines resumes normal imports early in 2026, Vietnam could see a quick rebound in shipments. Prices would stabilize, and total volume might climb back above 8.5 million tons. Even then, the price recovery may take time because global markets are still soft.

Scenario Two: The Ban Continues or Returns

If the Philippines extends or reintroduces restrictions, Vietnam will need to commit fully to diversification. Exporters will keep redirecting shipments to Africa and the Middle East. Total volume might stay around 7.5 to 8 million tons. Revenue could remain under pressure.

Scenario Three: Vietnam Formally Reduces Rice Production

The government could use this moment to push long-term changes. This might include reducing rice acreage, expanding aquaculture, developing specialty rice zones, and building branded rice supply chains. These changes would likely create a more stable industry but would also reduce total export volume.

Conclusion and Final Verdict

Vietnam’s rice export decline in 2025 is not simply the result of a policy decision in another country. The Philippines import ban accelerated a downturn that was already developing due to global price weakness, increased competition, and long-term structural pressures in Vietnam’s agricultural sector. The 11.5 percent fall in projected exports reflects both immediate market shocks and deeper challenges. Yet it also creates an opportunity for Vietnam to rethink its rice strategy. A shift toward higher-value rice, more diversified markets, and smarter production planning could make the country’s rice industry more resilient.

What happens next depends on global demand, the policy decisions of major buyers, and how quickly Vietnam can adapt. But one thing is clear. The industry is moving into a new era where quantity is no longer the only measure of success. Quality, branding, and strategic diversification will decide Vietnam’s future place in the global rice market.

For more insights into the latest Vietnam import-export data, or to search live data on Vietnam rice exports by country, visit VietnamExportdata. Contact us at info@tradeimex.in for customized trade reports, market insights, and a verified database of the top rice exporters in Vietnam, as per your needs.

Share

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0