Steel Import Data of Vietnam: Vietnam Steel Imports by Country & Top Steel Importers Data 2025

Discover insights into Vietnam steel import data for 2024–25, including top steel importers, major supplier countries, & trade trends shaping the industry.

Vietnam’s steel market has entered a defining phase. The country’s rapid industrialization, booming infrastructure projects, and growing manufacturing base have kept its steel demand surging, but local production still falls short in several critical categories. As a result, Vietnam has become one of Asia’s top steel importers, relying heavily on supply from regional heavyweights like China, Japan, and South Korea. According to the Vietnam import data and Vietnam customs import data of steel, the total value of Vietnam steel imports reached a record high $14.84 billion in 2024, a 19% increase from the previous year. According to Vietnam's steel import data and Vietnam customs data, Vietnam imported steel worth $4.3 billion in the first two quarters of 2025.

Vietnam is the 8th largest steel importer in the world, as per the global trade data. About 17.71 million metric tons of finished steel were imported by Vietnam in 2024, a 32.9% increase over the year before. Both an increase in steel output and a notable increase in domestic consumption were the main drivers of steel imports into Vietnam.

The years 2024 and 2025 marked a major turning point. After a record-breaking import surge in 2024, the early months of 2025 are showing a slowdown, influenced by shifting global prices, domestic policy interventions, and trade defense measures. Below is a detailed look at Vietnam’s steel import performance, key suppliers, and what the data reveals about the structure of the country’s steel industry.

Vietnam’s Steel Import Performance in 2024-25

In 2024, Vietnam imported approximately 17.7 million metric tons of steel, representing a jump of about 33% compared to 2023. The import value for the year crossed US$14.8 billion, the highest level recorded to date, as per the reports of the Vietnam Steel Association (VSA).

The first ten months of 2024 alone saw imports of around 15 million metric tons, with a total value of over US$10.48 billion. Compared to the same period in 2023, import volumes were up by 38%, while the value increased by roughly 23%. This gap between volume and value growth suggests that average import prices were declining, largely because of abundant, cheap steel flooding in from China.

In 2025, however, the momentum has softened. During the first half of 2025, Vietnam imported about 7.6 million metric tons, down nearly 8% year-on-year. Lower construction demand, slower industrial activity, and the introduction of anti-dumping duties on certain steel products have all contributed to this cooling trend.

Vietnam Steel Imports by Country: Where Does Vietnam Import Steel From?

Vietnam's steel imports come from a diverse range of countries. China stands out as the primary source of steel imports for Vietnam, followed by South Korea, Japan, and Taiwan. These countries cater to Vietnam's steel demand, providing a mix of raw materials and finished products to fuel the country's construction and manufacturing industries. Vietnam's strategic geographical location and growing economy make it an attractive market for steel exporters worldwide, further diversifying the sources of steel imports into the country. The top 10 import partners for Vietnam steel imports by country, as per the Vietnam shipment data and steel import statistics for 2024-25, include:

1. China: $7.57 billion (51%)

Unsurprisingly, China is the largest exporter of steel to Vietnam, accounting for a whopping 51% of the total steel imports in the country, as per the customs data on Vietnam steel imports from China by HS code. China has a massive steel production capacity and offers competitive prices, making it an attractive source for Vietnam's steel needs.

2. Japan: $2.51 billion (16.9%)

Japan is another key player in Vietnam's steel import market, contributing 16.9% of the total steel imports, as per the data on Vietnam steel imports from Japan. Known for its high-quality steel products, Japan has a strong presence in the Vietnamese market, particularly in the automotive and electronics industries.

3. South Korea: $1.30 billion (8.8%)

South Korea holds an 8.8% share in Vietnam's steel import market, offering a wide range of steel products to cater to the country's diverse industrial requirements. With advanced technology and efficient production processes, South Korean steel is highly sought after in Vietnam.

4. Indonesia: $1.26 billion (8.5%)

Indonesia is a significant player in Vietnam's steel import market, accounting for 8.5% of the total imports. The country's proximity to Vietnam, coupled with competitive pricing, makes it a preferred source for steel products in various sectors.

5. Taiwan: $642.97 million (4.3%)

Taiwan holds a 4.3% share in Vietnam's steel import market, providing a diverse range of steel products to meet the country's industrial demands. With a focus on innovation and quality, Taiwanese steel products are highly sought after by Vietnamese businesses.

6. India: $241.69 million (1.6%)

India is a growing player in Vietnam's steel import market, contributing 1.6% of the total imports. With a focus on value-added steel products, India offers competitive pricing and a diverse product range to meet Vietnam's ever-evolving steel requirements.

7. USA: $238.81 million (1.6%)

The USA holds a 1.6% share in Vietnam's steel import market, supplying a wide range of high-quality steel products to the country. Despite being a smaller player compared to other countries, the USA's reputation for superior quality steel makes it a preferred choice for certain industries in Vietnam.

8. Malaysia: $218.65 million (1.5%)

Malaysia is a key supplier of steel to Vietnam, accounting for 1.5% of the total imports. With a focus on sustainability and efficiency, Malaysian steel products are in high demand in Vietnam's construction and manufacturing sectors.

9. Hong Kong: $204.23 million (1.4%)

Hong Kong holds a 1.4% share in Vietnam's steel import market, offering a wide range of steel products to cater to the country's diverse industrial needs. With a focus on quality and reliability, Hong Kong steel is a preferred choice for many Vietnamese businesses.

10. Australia: $158.48 million (1.1%)

Australia is a minor player in Vietnam's steel import market, contributing 1.1% of the total imports. Despite its smaller market share, Australia's reputation for high-quality steel products makes it a preferred choice for specific industries in Vietnam.

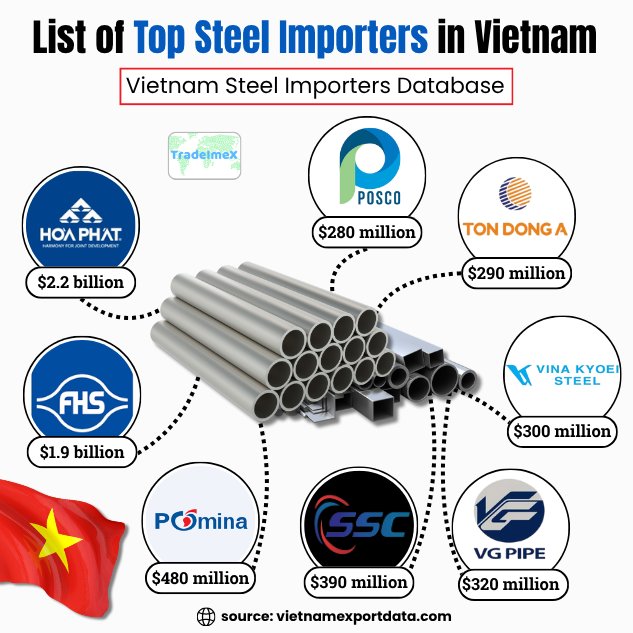

List of Top Steel Importers in Vietnam: Vietnam Steel Importers Database

The Vietnam Steel Importers Database provides a comprehensive and detailed overview of the key players in the steel import industry in Vietnam. This database aims to equip businesses with valuable insights into the market, allowing them to make informed decisions and establish successful partnerships within the steel import sector. The leading steel importers in Vietnam, as per the Vietnam steel importers data and steel buyers list for 2024-25, include:

|

Company |

Approximate Import Value (2024) |

Top Imported Steel Types |

Top Import Sources |

|

$2.2 billion |

Hot-rolled coil, billets, iron ore (plus some rolled steel) |

China, India, Australia |

|

|

Formosa Ha Tinh Steel Corporation |

$1.9 billion |

Slabs, rolled steel, coke |

Brazil, Japan, Australia |

|

Pomina Steel Corporation |

$480 million |

Scrap steel, coils, alloy steel |

South Korea, Japan, the United States |

|

Southern Steel Company (SSC) |

$390 million |

Billets, cold-rolled coils, construction-grade steel |

Russia, China, India |

|

VG PIPE (Vietnam Germany Steel Pipe Co.) |

$320 million |

Galvanized/coated steel products, steel pipes |

Taiwan, Malaysia, South Korea |

|

Vina Kyoei Steel Ltd. |

$300 million |

Billets, wire rods, long products |

Japan, Thailand, Indonesia |

|

Ton Dong A Corporation |

$290 million |

Coated flat steel, cold-rolled coils, substrates |

India, Japan, China |

|

POSCO Vietnam |

$280 million |

Hot-rolled and cold-rolled steel |

South Korea |

|

Maruichi Sun Steel Joint Stock Co. |

$240 million |

Precision tubes, coated steel |

Japan, Taiwan |

|

Viet Y Steel Company Ltd. |

$220 million |

Rebar, billets, long product steel |

China, Turkey, Russia |

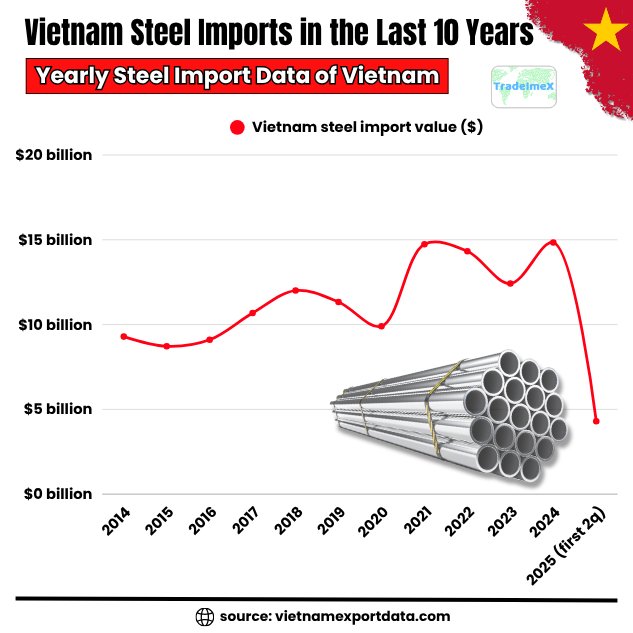

Vietnam Steel Imports in the Last 10 Years: Yearly Steel Import Data of Vietnam

|

Year of Imports |

Vietnam steel import value ($) |

|

2014 |

$9.29 billion |

|

2015 |

$8.72 billion |

|

2016 |

$9.10 billion |

|

2017 |

$10.68 billion |

|

2018 |

$12.01 billion |

|

2019 |

$11.33 billion |

|

2020 |

$9.90 billion |

|

2021 |

$14.74 billion |

|

2022 |

$14.32 billion |

|

2023 |

$12.42 billion |

|

2024 |

$14.84 billion |

|

2025 (first 2 quarters) |

$4.30 billion |

Vietnam Steel Import Volumes and Value Over Time

The historical pattern underscores how 2024 was an outlier in terms of growth.

|

Year |

Import Volume (Million Tons) |

Year-on-Year Change |

Import Value (US$ Billion) |

Year-on-Year Change |

|

2022 |

11.6 million tons |

– |

$14.3 billion |

– |

|

2023 |

13.3 million tons |

+14% |

$12.4 billion |

–12% |

|

2024 |

17.7 million tons |

+33% |

$14.8 billion |

+19% |

|

H1 2025 |

7.6 million tons |

–7.9% |

$4.3 billion |

–6.5% |

The record import volumes in 2024 were driven by strong domestic consumption and low global prices. Yet by mid-2025, the market began to rebalance as trade restrictions took hold and inventories grew faster than end-user demand.

Vietnam’s Top Steel-Supplying Countries

Vietnam’s steel import profile is highly concentrated. Three countries, China, Japan, and South Korea, supply nearly 90% of the total imported steel. The rest comes from a mix of regional sources such as Indonesia, Taiwan, and India.

China: The Dominant Supplier

China is the undisputed leader in Vietnam’s steel imports. In 2024, China supplied approximately 11.9 million metric tons, making up about two-thirds of Vietnam’s total steel imports. The import value was around US$7.5 billion, an increase of more than 30% from 2023.

Hot-rolled coil (HRC) is the centerpiece of these imports. Around 70-75% of all HRC imported by Vietnam originates from China. This material forms the foundation for producing cold-rolled, coated, and pre-painted steels, products that local mills like Hoa Phat and Formosa Ha Tinh cannot fully supply in volume or grade diversity.

China’s pricing advantage is formidable. Its HRC is often US$30-70 per ton cheaper than similar material from Japan or South Korea. However, this price gap has also triggered domestic concerns over dumping and market disruption. Vietnamese producers argue that Chinese mills are oversupplying the market with underpriced steel, eroding the profitability of local operations.

Japan: Supplier of Specialty Steel and Scrap

Japan holds the second position among Vietnam’s steel suppliers, with imports totaling about 1.7 million metric tons in 2024. These include both high-grade finished steel products and large volumes of steel scrap. In the first half of 2025 alone, imports from Japan reached around 1.2 million metric tons.

Japanese steel is recognized for its superior quality, particularly for automotive-grade and high-tensile applications, but it commands a higher price. Japanese scrap also plays a critical role in feeding Vietnam’s growing electric arc furnace industry.

South Korea: Consistent and Reliable

South Korea supplied about 1.05 million metric tons of steel to Vietnam in 2024, with a total import value of roughly US$1.3 billion. By the first half of 2025, the volume stood at around 0.7 million metric tons.

Korean mills specialize in coated, galvanized, and cold-rolled steels that cater to Vietnam’s manufacturing and appliance industries. Their share of total imports remains stable, even as competition from China intensifies.

Indonesia and Taiwan: Rising Regional Players

Indonesia has become an increasingly important source, exporting nearly 0.7 million tons of steel to Vietnam in the first half of 2025. This rapid growth reflects Indonesia’s expanding production capacity and logistical proximity to Vietnam.

Taiwan’s exports are smaller, totaling around 0.4 million tons in the same period, but the country remains a key supplier of cold-rolled and coated products.

Other Sources

Smaller volumes of steel arrive from India, Malaysia, Thailand, and Russia, but each contributes less than 2% of total imports. These sources tend to fluctuate depending on freight costs, tariffs, and market prices.

Steel Imports by Product Type

Vietnam imports a wide range of steel products, but three categories account for most of the total: hot-rolled coil (HRC), galvanized/coated steel, and steel scrap.

Hot-Rolled Coil (HRC)

HRC is the backbone of Vietnam’s steel imports. It represented over 70% of total steel import volume in 2024, with roughly 12 million tons imported.

Domestic capacity, mainly from Formosa Ha Tinh Steel and Hoa Phat Dung Quat, meets only about 55% of total HRC demand. The remaining 45% must be imported, primarily from China.

Average import prices for HRC hovered around US$550-580 per ton in 2024, significantly below domestic prices. This gap made imported HRC more attractive for downstream processors, even after accounting for logistics and duties.

Galvanized and Coated Steel

Vietnam imported about 1.4-1.6 million tons of galvanized and pre-painted steel in 2024, an increase of more than 20% from 2023. These products are essential in construction, roofing, and home appliance manufacturing.

Most coated steel imports come from China, Japan, and South Korea. However, domestic coated steel producers have voiced concern that these imports are being sold 10-15% below fair market prices, undermining local competitiveness.

Construction Steel (Long Products)

Rebar, wire rod, and structural steel imports are comparatively smaller. In 2023, Vietnam imported about 1.3 million tons of these products, with a modest uptick in 2024. Domestic production largely satisfies demand in this segment, leaving imports to fill niche gaps.

Steel Scrap

Scrap is a vital feedstock for electric arc furnace (EAF) operations in Vietnam. In 2024, scrap imports reached approximately 4.9 million tons, up 14% year-on-year. December 2024 alone saw over 600,000 tons of imported scrap.

The main suppliers of scrap are Japan, the United States, Hong Kong, and Australia. Rising scrap imports reflect Vietnam’s shift toward recycling-based production, but also highlight concerns about scrap quality and processing standards.

Steel Import Price Trends and Market Impact

Despite surging import volumes, average steel import prices fell in 2024 due to global oversupply and aggressive Chinese export pricing.

-

Average import price (Jan–Apr 2024): US$723 per ton

-

Average import price (2023): US$780 per ton

-

China-origin steel: US$30–50 per ton cheaper than alternatives

Lower prices benefited downstream manufacturers, such as machinery and appliance exporters, but squeezed margins for domestic steel producers. As a result, local mills reduced capacity utilization and delayed investment in expansion projects.

Trade Balance and Economic Impact

Vietnam’s steel sector has consistently run a trade deficit. In 2024, the country exported about US$8 billion worth of finished steel, while imports exceeded US$10.5 billion, creating a deficit of roughly US$2.5 billion.

This import-heavy structure exposes Vietnam to several vulnerabilities:

-

Overdependence on Chinese supply chains

-

Exposure to global price fluctuations

-

Pressure on domestic employment and profitability

However, it also brings advantages. Cheaper steel imports lower production costs for key downstream industries, construction, shipbuilding, and mechanical engineering, enhancing Vietnam’s competitiveness in export manufacturing.

Trade Policy and Government Response

The record-high imports of 2024 led to growing unease among local producers and policymakers. The Vietnamese government, through the Ministry of Industry and Trade (MOIT), has begun tightening trade controls and introducing defensive measures.

In February 2025, Vietnam imposed a temporary anti-dumping tariff on hot-rolled coil imports from China, effective for 120 days. The measure aimed to counteract underpriced imports that were distorting market dynamics. Authorities also reviewed coated and galvanized steel imports from China and South Korea, following claims that these products were being dumped at margins of 10–15%. Additional safeguard reviews for cold-rolled products are under consideration.

These policy shifts mark the beginning of a more protective phase for Vietnam’s steel sector, balancing open trade with industrial self-defense.

Domestic Supply and Import Dependency

Even with rising domestic production, Vietnam still relies heavily on imported steel for specific product types. The following table summarizes the estimated supply-demand gap as of 2024:

|

Product Type |

Domestic Capacity (Million Tons) |

Domestic Demand (Million Tons) |

Import Dependency |

|

Hot-Rolled Coil (HRC) |

7.5 million tons |

13 million tons |

45% |

|

Cold-Rolled/Coated Steel |

10 million tons |

11 million tons |

10% |

|

Long Products (Rebar, Rod) |

14 million tons |

12 million tons |

Surplus |

|

Steel Scrap (Raw Material) |

4 million tons |

5 million tons |

100% |

While domestic mills are expanding, especially in flat products, closing the import gap will take time and significant capital investment.

2025 Outlook and Market Trends

The first half of 2025 has signaled a moderation phase after the import boom of 2024.

-

Total imports fell by about 8% year-on-year.

-

Imports from China declined slightly as tariffs took effect.

-

Japan, South Korea, and Indonesia increased their market shares.

-

Scrap imports grew further, indicating stronger recycling activity.

-

Average steel prices began to stabilize globally, hinting at a gradual rebalancing of supply and demand.

Overall, 2025 is shaping up to be a year of adjustment rather than expansion. The balance between domestic production, import affordability, and policy protection will determine how Vietnam’s steel market evolves.

Strategic Implications

For policymakers, the priority is diversification. Reducing overreliance on Chinese steel is critical to ensuring long-term supply stability. Expanding trade relations with Japan, Korea, and Indonesia, while fostering domestic investment, will strengthen resilience.

For domestic producers, innovation and efficiency are essential. Competing on cost is difficult against Chinese mills; success will come from moving up the value chain into specialized and high-strength steels, as well as from embracing green production technologies.

For traders and importers, policy awareness is now crucial. Anti-dumping duties and safeguard measures can shift sourcing patterns overnight. Maintaining flexibility across multiple suppliers will be a key competitive advantage.

Conclusion and Final Thoughts

In conclusion, Vietnam’s steel import data from 2024-25 paints a vivid picture of transformation. Imports reached record highs in 2024, with nearly 17.7 million tons of steel entering Vietnam, dominated by China’s 51% market share. Prices declined, fueling downstream growth but straining local mills.

In 2025, the trend is cooling. Tariffs and trade measures are reshaping import flows, while domestic producers are preparing to defend their market position. The long-term outlook remains one of growth, but growth moderated by the need for balance between open trade & industrial security. Vietnam’s steel market is now standing at a crossroads: one path leads to continued import reliance, the other toward sustainable domestic self-sufficiency. How policymakers and producers manage this transition will determine whether Vietnam remains an import-heavy market or evolves into a regional steel powerhouse in the decade ahead.

We hope you liked our interactive blog report on the Vietnam steel import data 2025. For more information on the latest Vietnam export-import data, or to search live data on Vietnam steel imports by country, visit VietnamExportdata. Contact us at info@tradeimex.in and get customized trade reports, market insights, and a verified database of the top steel importers & buyers in Vietnam, as per your requirements.

Share

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0